If you own a cargo e-bike or electric trike, you already know these machines are serious investments. So understanding what is e-bike cargo insurance isn’t just a paperwork exercise. It’s the difference between recovering from theft or an accident and absorbing a $3,000 to $8,000 loss out of pocket. Most cargo e-bike owners assume their homeowners or renters policy has them covered. It usually doesn’t. This guide breaks down exactly what cargo insurance for e-bikes covers, where standard policies fall short, and how to choose the right protection for your specific situation.

E-bike cargo insurance covers theft, accident damage, and third-party liability protection built specifically for electric cargo bikes. This isn’t the same as a basic bicycle rider on your home policy. Specialist policies treat your cargo e-bike as the complex, high-value machine it actually is.

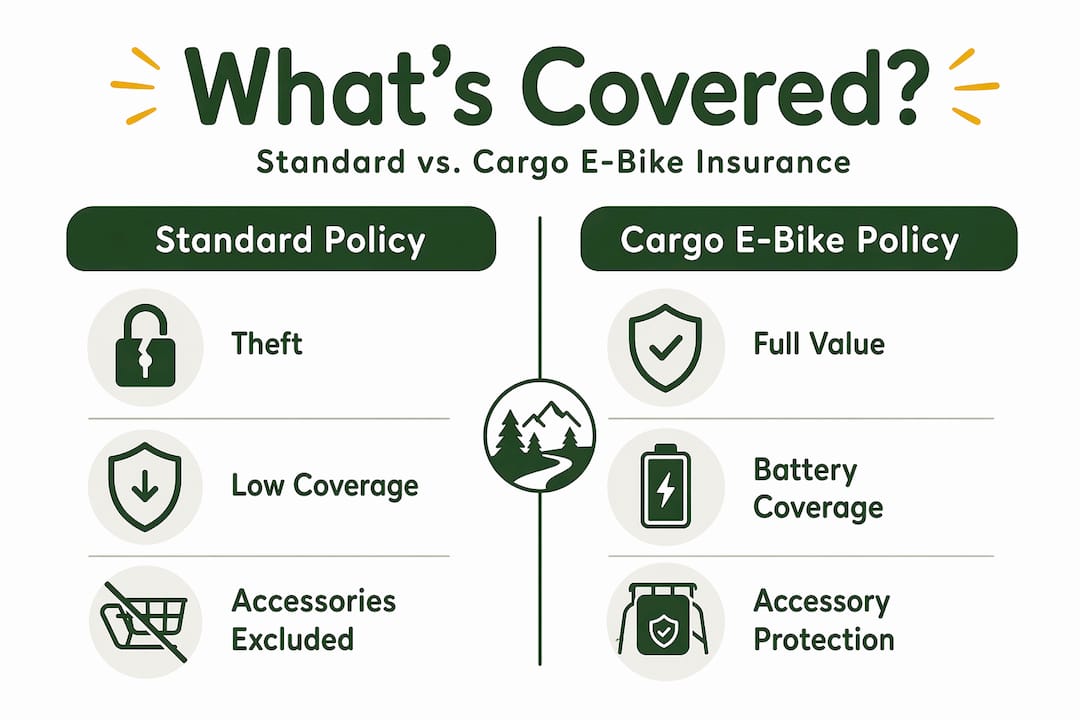

Here’s what a solid e-bike cargo insurance policy typically includes:

One thing that surprises many riders is how battery coverage actually works. Battery classification affects coverage significantly. If your insurer treats the battery as a detachable accessory rather than an integral part of the bike, battery-only theft may not be covered under the main policy. Always ask your insurer directly how they classify the battery before you sign anything.

Standard bike insurance policies are not designed for cargo e-bikes. They often cap payouts at values that don’t reflect the real cost of a longtail cargo bike or an electric trike. Specialist cargo e-bike insurance closes that gap by covering the full replacement value of a machine that might cost more than some used cars.

Pro Tip: Ask your insurer whether accessories like cargo bags, child seats, and rear racks are covered under the main policy or require a separate rider. These add-ons can easily total several hundred dollars.

Many riders discover the hard way that their homeowners or renters policy doesn’t actually protect their cargo e-bike. Homeowners policies likely don’t cover e-bike theft or damage adequately, especially off-premises. Here’s a direct comparison of what you get with each option:

The liability gap is the issue most people overlook entirely. Homeowners liability typically excludes motor vehicles, and many Class 2 and Class 3 e-bikes fall into that category under policy language. If you cause an accident on your cargo e-bike and injure someone, you could be personally liable for medical bills and legal costs with zero coverage from your home policy.

“Homeowners or renters insurance usually provides inadequate e-bike coverage, encouraging uptake of standalone policies geared to e-bike risks.” — USA Cycling

There’s also the deductible problem. Filing an e-bike theft claim under your homeowners policy means triggering your home deductible, which is often $1,000 or higher. A standalone e-bike policy typically carries a much lower deductible and won’t affect your homeowners premium when you file a claim.

This is where most cargo e-bike owners get tripped up. Having insurance isn’t enough. You have to follow your insurer’s specific security requirements, or your theft claim can be denied before it even gets reviewed.

Here’s what most specialist insurers require for theft claims on cargo e-bikes:

Pro Tip: Take a photo of your locked bike every time you leave it in a public place. That 10-second habit creates a timestamped record of your lock setup, which can be the deciding factor in a disputed claim.

Choosing the right coverage comes down to four practical factors: your bike’s value, how you use it, your risk tolerance, and what you’re already paying for elsewhere.

This distinction matters more than almost anything else in your policy. Actual cash value pays out what your bike is worth at the time of the claim, after depreciation. A two-year-old cargo e-bike that cost $4,500 might only pay out $2,800 under an actual cash value policy. Replacement cost coverage pays what it actually costs to replace the bike with a comparable model today. For cargo e-bikes, always choose replacement cost.

For most cargo e-bike owners, a standalone specialist policy is the better choice. Dedicated e-bike insurance partnerships like Tern and BikeInsure in 2026 show the market moving toward purpose-built coverage that addresses theft, transit damage, and riding accidents in one package. These policies are designed around how cargo bikes are actually used.

Here’s a quick checklist when evaluating any cargo e-bike insurance policy:

If you use your cargo e-bike for deliveries or any commercial purpose, personal insurance policies may not cover you during work hours. Commercial e-bike policies exist specifically for this use case. Check whether your policy explicitly covers commercial use before assuming you’re protected on the job. The FIIDO T2 longtail cargo e-bike is a great example of a bike that works beautifully for both personal and light commercial hauling. A bike like that deserves coverage that matches how you actually ride it.

I’ve talked to a lot of cargo e-bike owners over the years, and the pattern I keep seeing is the same. People spend real money on a quality machine, then treat insurance as an afterthought.

The battery coverage issue is the biggest “gotcha” I’ve encountered. Riders assume the battery is covered because it’s attached to the bike. But how the insurer classifies the battery determines whether a standalone battery theft is covered at all. I’ve seen riders lose $800 to $1,200 on a stolen battery because they never asked this one question before buying their policy.

The liability gap is just as serious. Most cargo e-bike riders I know have never thought about what happens if they hit a pedestrian or cause a car accident. A single injury claim can run into tens of thousands of dollars. A standalone policy with proper liability limits costs a fraction of that risk.

My practical advice: document everything before something goes wrong. Serial numbers, purchase receipts, photos of the bike from multiple angles, and a record of your lock setup. Keep these in cloud storage so they’re accessible from anywhere. When a claim happens, the riders who get paid quickly are the ones who show up with organized documentation. The ones who get denied or delayed are the ones who assumed the insurer would just take their word for it.

— Andres

At Quality Quest Bikes, we carry cargo e-bikes and trikes built for real-world use. Whether you’re hauling groceries, running deliveries, or replacing your car for daily errands, the right bike deserves proper protection.

The ECOTRIC 48V 750W electric tricycle is one of our most popular cargo-capable models, and it’s exactly the kind of investment that warrants a standalone insurance policy. For riders who want a long-range option with a full cargo kit, the EAHORA Cupid e-bike ships with everything you need to start hauling. Both bikes are available with fast and free shipping, no hidden costs. Browse our full cargo e-bike lineup at Qualityquestbikes and pair your purchase with the right insurance from day one.

E-bike cargo insurance typically covers theft, accidental damage, and third-party liability for electric cargo bikes, including the motor and battery when lock requirements are met.

Most homeowners and renters policies provide inadequate coverage for cargo e-bikes, often excluding off-premises theft, accidental damage, and liability for motorized bikes.

Claims are most often denied because the bike was not locked with an approved lock standard, was not secured through the frame to an immovable object, or lacked a police report filed promptly after the theft.

Personal e-bike insurance policies typically exclude commercial use. If you use your cargo e-bike for deliveries or paid work, you need a policy that explicitly covers commercial riding to be protected on the job.

Replacement cost pays what it costs to buy a comparable bike today, while actual cash value pays the depreciated worth of your bike at the time of the claim. Replacement cost is almost always the better choice for cargo e-bikes.

You deserve quality products at fair prices. Period.

Which is why we offer no sales tax and price matching

Orders include free shipping and are dispatched within 1 -2 business days.

Exceptions apply.

We want you to be enthusiastically satisfied with your order, have any questions?

Your support keeps our wheels rolling!

We’re more than just a store — we’re part of a growing local community of utility bike and trike enthusiasts who are passionate about creating positive change.

Subscribe and be the first to learn about our news and promotions

Your cart is empty